The UK pawnbroking industry is far larger and more regulated than many realise. With 208 established businesses generating over £324 million in annual revenue.aspx), pawnbroking offers secured loans that don’t affect your credit score. Yet misconceptions persist about authenticity, value and regulation. Whether you’re considering pawning jewellery for quick cash or buying pre-owned pieces, understanding hallmarks, FCA oversight and pricing dynamics ensures you secure genuine value. This guide walks you through the regulatory framework, authentication methods and practical considerations for navigating pawnbroking and pre-owned jewellery purchases with confidence.

Table of Contents

- Key takeaways

- Regulation and trust in UK pawnbroking

- Understanding hallmarks and jewellery authenticity

- Buying pre-owned jewellery from pawnbrokers: value and considerations

- Navigating pawnbroking loans: benefits, risks and comparisons

- Discover trusted pawnbroking and pre-owned jewellery services

- Frequently asked questions about pawnbroking and pre-owned jewellery

Key Takeaways

| Point | Details |

|---|---|

| Regulatory framework | The UK pawnbroking sector is tightly regulated with FCA authorisation and transparent loan terms to protect consumers. |

| Hallmarks verify authenticity | Hallmarks confirm precious metal content and the Hallmarking Act mandates legal marks on jewellery above specified weights. |

| Pre owned jewellery value | Pre owned pieces can offer value but buyers should verify hallmarks and seller credibility. |

| Loans and APR | Loans are secured against pledged items and require explicit disclosure of APR and redemption periods. |

| Pawning keeps ownership | Pawning keeps ownership of the item while providing a cash loan rather than a sale. |

Regulation and trust in UK pawnbroking

Pawnbroking operates under strict legal frameworks designed to protect consumers. The Consumer Credit Act 1974 forms the foundation of pawnbroking regulation, requiring every pawnbroker to obtain FCA authorisation before conducting business. This isn’t optional paperwork. Without authorisation, operating as a pawnbroker constitutes a criminal offence.

The National Pawnbrokers Association represents 97% of the UK pawnbroking trade, promoting ethical standards and best practice across the industry. FCA regulation ensures pawnbrokers follow transparent lending practices.aspx), including clear documentation of loan terms, interest rates and redemption periods. This regulatory oversight distinguishes legitimate pawnbrokers from unregulated lenders.

Loans secured against pawnbrokered goods don’t impact your credit score because they’re collateralised transactions. The pawnbroker holds your item as security, so there’s no credit check required. In 2023, approximately 900,000 loans totalling £865 million were issued across the UK pawnbroking market. These figures demonstrate the scale of demand for secured, short-term lending.

Regulation covers several critical areas:

- Transparent disclosure of APR and total repayment amounts before agreement

- Minimum redemption periods allowing borrowers time to repay

- Secure storage and insurance of pledged items

- Clear procedures for item valuation and loan calculation

- Documented processes for unredeemed goods after the redemption period expires

The regulatory framework creates accountability. If you pawn jewellery, the pawnbroker must provide a pawn ticket detailing the loan amount, interest rate, redemption date and item description. This document serves as your legal proof of ownership and loan terms. Keep it safe, as you’ll need it to reclaim your item.

“FCA authorisation isn’t just bureaucracy. It means pawnbrokers must maintain professional standards, proper insurance and transparent pricing. This protects you from predatory lending and ensures your pledged items are handled responsibly.”

When considering cash loans on jewellery, verify the pawnbroker displays their FCA authorisation number prominently. You can check authorisation status on the FCA register. Legitimate businesses welcome this scrutiny because it demonstrates their commitment to regulatory compliance.

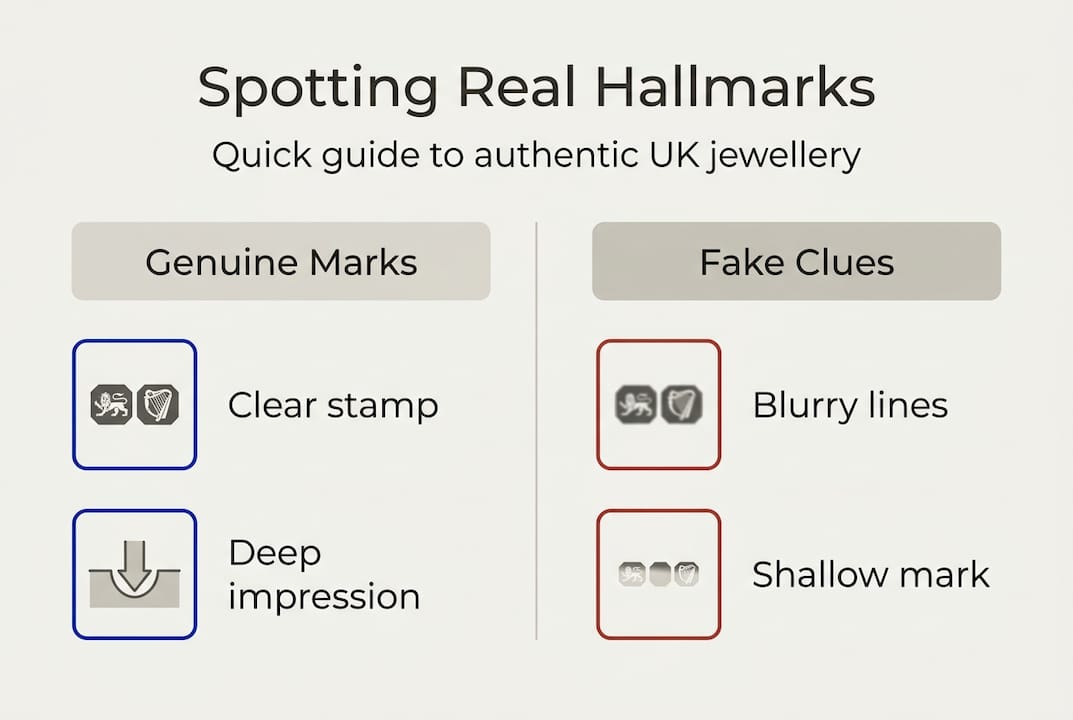

Understanding hallmarks and jewellery authenticity

Hallmarks provide legal proof of precious metal content. The Hallmarking Act 1973 mandates that gold, silver, platinum and palladium jewellery over specific weight thresholds must carry official hallmarks before sale. Selling unhallmarked precious metal jewellery above these weights is illegal, carrying fines and potential prosecution.

Four UK assay offices regulate hallmarking: London, Birmingham, Sheffield and Edinburgh. Each stamps jewellery with distinctive marks confirming metal type, purity and origin. A complete hallmark typically includes four elements: the sponsor’s mark identifying the manufacturer, the standard mark showing purity, the assay office mark and the date letter.

Understanding purity marks prevents costly mistakes:

- 375 indicates 9 carat gold (37.5% pure gold)

- 585 indicates 14 carat gold (58.5% pure gold)

- 750 indicates 18 carat gold (75% pure gold)

- 916 indicates 22 carat gold (91.6% pure gold)

- 925 indicates sterling silver (92.5% pure silver)

- 950 indicates platinum or higher grade silver

Items under 1 gram are exempt from hallmarking requirements, but this rarely applies to valuable jewellery pieces. Delicate chains or small earrings might fall below this threshold, yet most pawnable or investment-worthy pieces exceed it.

Pro Tip: Use a jeweller’s loupe or magnifying glass to examine hallmarks closely. Genuine stamps appear crisp and deeply impressed. Fake or poorly struck marks often look fuzzy, shallow or inconsistent. If you can’t locate hallmarks on a supposedly precious metal item, request professional verification before purchase or pawning.

Counterfeit jewellery poses serious risks beyond financial loss. Selling fake hallmarked items constitutes fraud under UK law. Buyers who unknowingly purchase fakes have limited recourse unless they can prove the seller knew about the deception. This makes buying from reputable, established jewellers essential.

| Metal type | Hallmark number | Purity percentage | Common uses |

|---|---|---|---|

| 9ct gold | 375 | 37.5% | Everyday jewellery, affordable pieces |

| 14ct gold | 585 | 58.5% | Mid-range jewellery, some imported pieces |

| 18ct gold | 750 | 75% | Fine jewellery, engagement rings, luxury items |

| 22ct gold | 916 | 91.6% | Traditional Asian jewellery, investment pieces |

| Sterling silver | 925 | 92.5% | Silver jewellery, cutlery, decorative items |

| Platinum | 950 | 95% | Premium jewellery, wedding bands |

When spotting fake gold jewellery, hallmarks provide your first line of defence. However, sophisticated fakes sometimes carry counterfeit hallmarks. Combine hallmark inspection with other tests: genuine gold doesn’t tarnish, feels heavier than base metals of similar size, and responds to magnet tests differently than plated items.

Buying pre-owned jewellery from pawnbrokers: value and considerations

Pre-owned jewellery from pawnbrokers offers substantial savings, but requires careful evaluation. Authenticated pre-owned diamond jewellery typically sells for 25-50% below retail prices, creating opportunities for savvy buyers. The key lies in verification and quality assessment.

Start with certificates. Reputable diamond jewellery should come with grading reports from recognised laboratories like GIA, HRD or IGI. These certificates detail the 4Cs: cut, colour, clarity and carat weight. Without certification, you’re relying solely on the seller’s word about diamond quality. That’s risky when spending significant money.

The 4Cs determine diamond value:

- Cut quality affects brilliance and light performance most dramatically

- Colour grades from D (colourless) to Z (light yellow), with D-F commanding premiums

- Clarity measures internal inclusions and external blemishes

- Carat weight indicates size, but doesn’t determine quality alone

Pro Tip: Don’t fixate on carat weight alone. A well-cut 0.9 carat diamond with excellent colour and clarity often looks more impressive and costs less than a poorly cut 1.0 carat stone with visible inclusions. Focus on overall visual impact rather than hitting specific carat milestones.

Condition assessment matters enormously for pre-owned pieces. Examine settings for loose stones, worn prongs or structural damage. Check clasps, hinges and joints on bracelets and necklaces. Surface scratches on gold can be polished out, but bent settings or damaged prongs require repair before wear.

Provenance adds value and authenticity. Documentation proving previous ownership, original purchase receipts or appraisal certificates strengthen confidence in authenticity. Pawnbrokers handling unredeemed pledges should provide basic provenance information when available.

| Purchase consideration | New retail jewellery | Pre-owned from pawnbrokers | What to verify |

|---|---|---|---|

| Price point | Full retail markup | 25-50% discount typical | Compare similar pieces across multiple sources |

| Certification | Usually included | Request certificates | GIA, HRD or IGI diamond reports |

| Condition | Pristine | Varies, may show wear | Inspect settings, clasps, stone security |

| Warranty | Manufacturer warranty | Limited or none | Clarify any guarantees offered |

| Authenticity risk | Minimal from reputable retailers | Requires verification | Check hallmarks, test metals, verify certificates |

| Customisation options | Full range available | Limited to existing piece | Consider modification costs if needed |

Reputable pawnbrokers provide professional appraisals and authentication before selling pre-owned jewellery. This protects both parties. Ask about their verification process. Do they employ qualified gemmologists? Do they test metals and verify hallmarks? Transparent answers indicate professionalism.

When you buy authenticated second hand jewellery, insist on documentation. A detailed receipt describing the item, metal content, stone specifications and any certifications creates legal protection if authenticity issues arise later. Verbal assurances mean nothing without paper trails.

Common pitfalls include:

- Accepting vague descriptions without specific metal content or stone grades

- Skipping independent appraisal for high-value purchases

- Ignoring structural damage that requires expensive repair

- Overlooking missing certificates for certified diamonds

- Failing to compare prices across multiple sellers

Navigating pawnbroking loans: benefits, risks and comparisons

Pawnbroking loans provide quick access to cash whilst retaining ownership of your valuables. Unlike selling, you can reclaim items after repaying the loan. This flexibility appeals when you need temporary funds but want to keep sentimental or valuable pieces long term.

However, interest rates vary dramatically, ranging from 20% to 150% APR depending on the pawnbroker, loan amount and item type. Jewellery comprises approximately 60% of all pawnbrokered collateral, reflecting its combination of high value, easy authentication and compact storage.

Before accepting a pawnbroking loan, follow these steps:

- Obtain valuations from multiple pawnbrokers to compare loan offers

- Calculate total repayment amount including all interest and fees

- Verify the redemption period and any extension options available

- Confirm storage and insurance arrangements for your pledged item

- Read all documentation thoroughly before signing anything

- Keep your pawn ticket secure as proof of ownership and loan terms

Luxury pawnbroking services often provide better terms for high-value items. Specialist luxury pawnbrokers understand fine jewellery, watches and precious metals more deeply than general pawnbrokers. They may offer lower interest rates, longer redemption periods and higher loan-to-value ratios because they can accurately assess and market premium items.

| Loan option | Typical APR range | Loan-to-value ratio | Redemption period | Best for |

|---|---|---|---|---|

| High street pawnbroker | 80-150% | 40-60% of value | 6 months standard | Quick small loans, everyday items |

| Luxury pawnbroker | 20-80% | 50-70% of value | 6-12 months, flexible | High-value jewellery, designer watches |

| Selling outright | N/A (not a loan) | 60-80% of value | Immediate, permanent | When you don’t need the item back |

| Personal loan (bank) | 3-30% | Unsecured | 1-5 years | Lower rates but requires credit check |

Short-term risks include losing your item if you can’t repay. Once the redemption period expires, the pawnbroker can sell your pledged goods to recover the loan. Extensions may be available, but these add more interest. Calculate whether you can realistically repay within the timeframe before pawning.

Loan paperwork creates value beyond the immediate cash. If you later decide to sell jewellery, having professional appraisal documents from a pawnbroker strengthens your negotiating position. It provides third-party verification of authenticity and value.

“Pawnbroking suits temporary cash needs when you’re confident about repayment. If you’re uncertain about repaying within the redemption period, selling outright to avoid accumulating interest might be wiser. Honest assessment of your financial situation prevents losing items to default.”

Compare pawnbroking against alternatives. Bank personal loans offer much lower interest rates but require credit checks and take longer to process. Selling jewellery outright provides immediate cash without repayment obligations but means permanent loss of the item. Each option suits different circumstances.

When considering where to sell jewellery if pawning isn’t right, explore established jewellers who specialise in pre-owned pieces. They often pay better prices than general pawnbrokers because they understand the resale market and can authenticate items accurately.

Discover trusted pawnbroking and pre-owned jewellery services

Navigating pawnbroking and pre-owned jewellery purchases demands expertise you can trust. Blackwell Jewellers combines over 20 years of family-run jewellery experience with FCA-regulated pawnbroking services across Kent and a comprehensive national online platform.

Every pre-owned piece undergoes rigorous inspection, authentication and hallmark verification by qualified jewellers before sale. This ensures you’re buying genuine items with transparent provenance and structural integrity. Whether you’re pawning jewellery for short-term cash or investing in authenticated pre-owned pieces, Blackwell Jewellers provides the accountability and craftsmanship that makes these transactions confident decisions.

Explore comprehensive guides on buying authenticated second hand jewellery and responsible cash loans to make informed choices backed by expert knowledge and regulatory compliance.

Frequently asked questions about pawnbroking and pre-owned jewellery

Do pawnbroking loans affect my credit score?

No, pawnbroking loans don’t impact credit scores because they’re secured against your pledged item rather than assessed through credit checks. The pawnbroker holds your jewellery as collateral, eliminating credit risk. This makes pawnbroking accessible even with poor credit history.

How do I verify hallmarks on pre-owned jewellery?

Use a jeweller’s loupe to examine stamps closely for crispness and depth. Genuine hallmarks appear sharply defined with consistent impression depth. Cross-reference the marks against official assay office guides to confirm they match legitimate patterns. For valuable pieces, request professional verification from a qualified jeweller or gemmologist.

What should I look for when choosing a pawnbroker?

Verify FCA authorisation by checking their registration number on the FCA register. Ask about their valuation process, storage security and insurance arrangements. Compare loan terms, APR rates and redemption periods across multiple pawnbrokers. Established businesses with transparent processes and professional premises indicate reliability.

What are the most common counterfeit jewellery warning signs?

Missing or poorly struck hallmarks signal potential fakes. Unusually low prices compared to similar authentic pieces suggest problems. Vague descriptions avoiding specific metal content or stone grades indicate lack of proper authentication. Sellers reluctant to provide certificates or allow independent appraisal raise red flags. When buying pre-owned gold, learn comprehensive fake detection methods including magnet tests and acid testing.

Can I negotiate pawnbroking loan terms?

Some flexibility exists, particularly with luxury pawnbrokers handling high-value items. Loan-to-value ratios, interest rates and redemption periods may be negotiable based on item quality and your relationship with the pawnbroker. However, regulatory requirements limit how much terms can vary. Always get final agreed terms documented in writing before accepting any loan.

Is buying pre-owned jewellery from pawnbrokers safe?

Buying from FCA-regulated pawnbrokers with established reputations provides reasonable safety when you verify authenticity properly. Check hallmarks, request certificates for diamonds, inspect condition thoroughly and compare prices across sources. Reputable pawnbrokers authenticate items before sale and provide documentation. Your diligence combined with their professional verification creates a secure transaction environment.