Facing an unexpected bill or emergency expense can feel overwhelming, especially when traditional credit options aren’t available or suitable. Many UK residents turn to their jewellery collections as a practical financial resource during these moments. Pawnbroking offers a regulated, straightforward way to access cash quickly using your valuables as collateral, without credit checks or lengthy approval processes. This guide walks you through obtaining cash loans on jewellery responsibly, from initial preparation through repayment, ensuring you understand your rights and protections throughout the process.

Table of Contents

- Key takeaways

- What you need to prepare before getting a cash loan on jewellery

- Step-by-step guide to obtaining a cash loan on your jewellery

- Common pitfalls and how to avoid them when pawning jewellery

- What to expect after the loan: repayment, renewals and item recovery

- Discover trusted pawnbroking services for your jewellery

- FAQs about cash loans on jewellery

Key Takeaways

| Point | Details |

|---|---|

| Regulated pawnbroking | Select FCA authorised pawnbrokers to ensure fair terms and regulatory protections. |

| Loan term length | Most loans run six to seven months with no credit checks. |

| Borrowing percentage | Lenders typically offer about 50 to 70 per cent of the item’s retail value. |

| Ownership upon repayment | Borrowers retain ownership if they repay the loan, otherwise the pledged items are sold to recover the debt. |

| Surplus returns | Any surplus from the sale above the loan value must be returned to borrowers. |

What you need to prepare before getting a cash loan on jewellery

Proper preparation makes the pawnbroking process smoother and protects your interests. Start by identifying which jewellery pieces you’re willing to use as collateral. Gold, silver, diamond pieces and hallmarked items typically secure better loan values. Gather any documentation proving ownership, such as purchase receipts, insurance certificates or valuation documents. These aren’t always mandatory but strengthen your position and can help secure better terms.

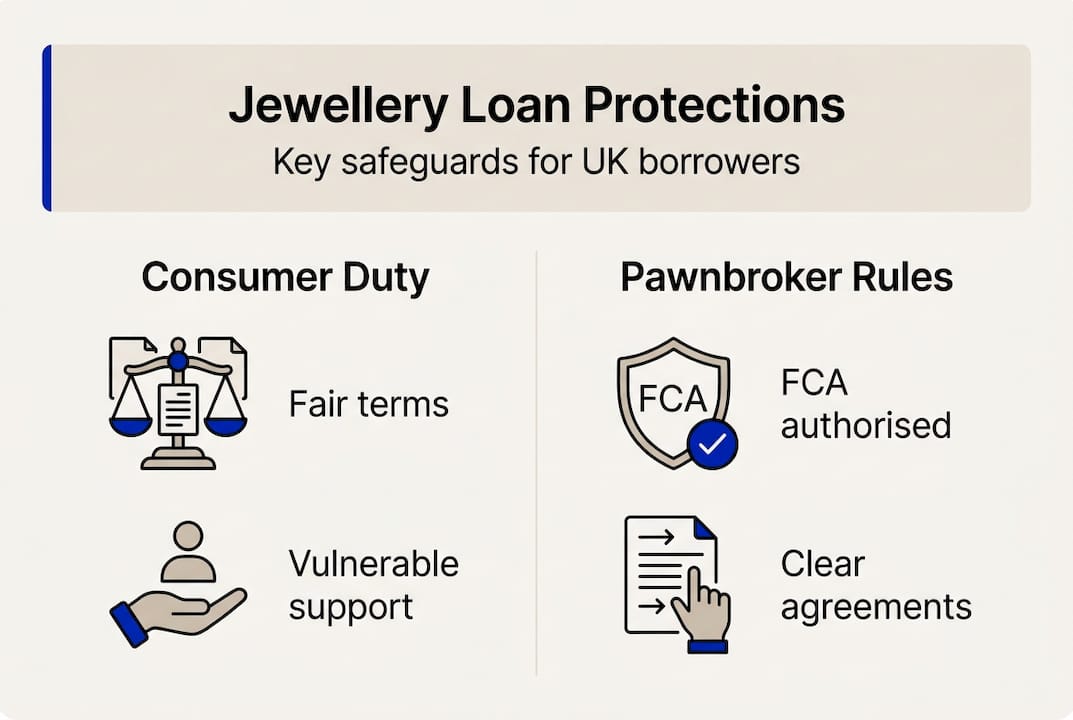

Verifying your chosen pawnbroker’s credentials is absolutely essential. Pawnbrokers must be FCA authorised, with pawnbroking regulated under the Consumer Credit Act. Members of the National Pawnbrokers Association follow a code of conduct ensuring fairness and transparency. Check the FCA register before committing to any agreement. This simple step protects you from unscrupulous operators and ensures you benefit from proper regulatory oversight.

Understanding standard loan conditions helps set realistic expectations. Most pawnbroking loans run for six to seven months, though terms vary between providers. You won’t face credit checks, making this option accessible regardless of your credit history. The amount you can borrow depends on your jewellery’s market value, current gold prices and the pawnbroker’s assessment criteria. Expect to receive between 50-70% of an item’s retail value, though this varies significantly.

Prepare the required documentation before your appointment. You’ll need valid photo identification such as a passport or driving licence. Proof of address dated within the last three months, like a utility bill or bank statement, is standard. Some pawnbrokers request additional ownership verification for high-value pieces. Having everything organised demonstrates professionalism and speeds up the process considerably.

The FCA’s Consumer Duty regulations provide important protections for vulnerable customers. Pawnbrokers must identify customers facing financial difficulties and offer appropriate support. This might include flexible repayment options, extended loan periods or signposting to debt advice services. Don’t hesitate to discuss your circumstances openly if you’re struggling financially.

If you’re considering online pawnbroking services, understand the shipping risks involved. Insured, tracked delivery is essential when sending valuable items. Confirm the pawnbroker’s insurance covers your jewellery during transit and whilst in their possession. Some borrowers prefer face-to-face transactions for peace of mind, particularly with sentimental or high-value pieces.

Pro tip: Before visiting a pawnbroker, research current gold and silver prices. Knowing approximate market values helps you assess whether loan offers are fair and reasonable.

Key preparation checklist:

- Identify suitable jewellery pieces with clear ownership

- Verify FCA authorisation and NPA membership

- Gather identification and proof of address

- Research current precious metal market prices

- Understand typical loan durations and terms

- Confirm insurance coverage for shipping if applicable

Learn more about cash lent on jewellery in the UK and how valuations work. The FCA’s guidance on pawnbroking offers detailed consumer protection information.

Step-by-step guide to obtaining a cash loan on your jewellery

The pawnbroking process follows a structured sequence designed to protect both parties. Understanding each stage helps you navigate the experience confidently and make informed decisions throughout.

Step 1: Item evaluation and loan offer. Visit the pawnbroker with your jewellery for professional assessment. The valuer examines each piece, checking hallmarks, testing precious metal content and assessing gemstone quality. They consider current market values and gold prices when calculating loan amounts. Cash loans on jewellery operate via pawnbroking, where you pledge items as collateral for short-term loans typically lasting six to seven months, with no credit checks required. The pawnbroker presents an offer based on this evaluation. You’re under no obligation to accept.

Step 2: Review and agree to loan terms. If you’re satisfied with the offer, carefully review all terms before signing anything. The agreement must clearly state the loan amount, interest rate, APR, loan duration and total repayment figure. Ask questions about anything unclear. Reputable pawnbrokers welcome enquiries and explain terms thoroughly. Pay particular attention to renewal policies and what happens if you can’t repay on time. This transparency prevents unpleasant surprises later.

Step 3: Provide identification and ownership proof. Present your photo identification and proof of address. The pawnbroker copies these documents and verifies their authenticity. If you have ownership documentation for the jewellery, provide it now. The pawnbroker creates a detailed description of each pledged item, often including photographs. Review this description carefully to ensure accuracy. This record protects both parties and facilitates item recovery when you repay the loan.

Step 4: Receive your cash loan. Once paperwork is complete, you receive the loan amount immediately. Payment methods vary but typically include cash, bank transfer or cheque. The pawnbroker provides a pawn ticket or receipt containing essential information: your details, item descriptions, loan amount, interest charges, repayment deadline and total amount due. Store this document safely as you’ll need it to reclaim your jewellery.

Step 5: Understand your repayment and renewal options. Your loan typically runs for six to seven months, though terms vary. You can repay early without penalties at most pawnbrokers. If you can’t repay by the deadline, discuss renewal options before the due date. Renewals extend the loan period but accrue additional interest. Some pawnbrokers allow partial payments to reduce the outstanding balance. Understanding these options gives you flexibility if circumstances change.

Pro tip: Always clarify the APR and all fees upfront. Whilst monthly interest rates might seem reasonable, annual percentage rates can be substantial. Knowing the true cost helps you budget effectively and compare different pawnbrokers if needed.

For insights into how professionals assess jewellery quality, explore the jewellery repair process, which reveals the detailed inspection methods experts use.

Common pitfalls and how to avoid them when pawning jewellery

Even with preparation, borrowers sometimes encounter problems that could have been prevented. Awareness of common mistakes helps you navigate pawnbroking safely and protect your valuable possessions.

High APRs represent the most significant financial risk. Whilst monthly interest rates of 3-5% seem manageable, they translate to substantial annual costs. A £500 loan at 4% monthly interest costs £20 monthly or £240 annually, resulting in a 48% APR. These rates make long-term borrowing expensive. Only use pawnbroking for genuine short-term needs and repay as quickly as possible to minimise interest charges.

Dealing with unauthorised or non-transparent pawnbrokers creates serious risks. Some operators aren’t properly regulated or deliberately obscure terms and conditions. Always verify FCA authorisation before proceeding. Avoid pawnbrokers who pressure you into agreements, refuse to provide written terms or seem evasive about fees and charges. These red flags indicate potential problems.

Misunderstanding what happens if you don’t repay causes unnecessary anxiety. If loans remain unpaid, items are sold, but your liability is capped at the item’s market value. Crucially, surpluses from sales exceeding the loan plus interest must be returned to you. Recent FCA interventions have improved surplus collection, with staff flags increasing returns by 44%. You won’t face debt collectors chasing additional payments if your jewellery sells for less than the loan amount.

Unclear renewal policies trap some borrowers in escalating debt cycles. Before accepting any loan, understand exactly how renewals work. Can you renew indefinitely? Are there limits on renewal periods? Do renewal fees differ from initial charges? Some pawnbrokers impose increasing fees for multiple renewals, making escape from the debt cycle progressively harder. Clarify these details upfront.

Failing to keep records and receipts creates problems when claiming surpluses or disputing valuations. Your pawn ticket is essential for reclaiming items and proving ownership. If the pawnbroker sells your jewellery and a surplus exists, you’ll need documentation to claim it. Store all paperwork safely and make copies for additional security.

“Understanding your rights under FCA regulation transforms pawnbroking from a risky gamble into a legitimate financial tool. The protections exist, but only if you know to claim them and choose regulated providers.”

Common mistakes to avoid:

- Underestimating total costs by focusing only on monthly interest rates

- Choosing pawnbrokers based solely on loan amounts without checking credentials

- Failing to read and understand all terms before signing agreements

- Losing pawn tickets or receipts needed for item recovery

- Not exploring renewal options before missing repayment deadlines

- Assuming you’ll owe additional money if items sell below loan value

Discover how jewellery is refurbished to understand the care professionals take with valuable pieces, which should mirror how pawnbrokers treat your pledged items.

What to expect after the loan: repayment, renewals and item recovery

Understanding post-loan processes helps you plan effectively and make informed decisions about repayment, renewals or accepting item forfeiture if necessary.

Repayment within the agreed six to seven month period is straightforward. Contact the pawnbroker before your deadline to arrange payment. Most accept cash, bank transfers or card payments. You’ll pay the original loan amount plus accumulated interest. Upon receipt, the pawnbroker returns your jewellery immediately. Inspect items carefully before leaving to ensure they match the original description and haven’t been damaged during storage.

Renewing loans provides flexibility when you can’t repay on time. Contact your pawnbroker before the deadline to discuss options. Responsible pawnbrokers offer renewals.aspx) with borrower liability capped and surpluses returned, following improved FCA regulatory standards. Renewal extends the loan period, typically for another six to seven months, but interest continues accruing. Some pawnbrokers allow you to pay just the interest to renew, whilst others require partial capital repayment. Clarify terms before agreeing to renewals to avoid unexpected costs.

If you decide not to repay or renew, the pawnbroker sells your jewellery to recover the loan. This isn’t necessarily catastrophic. Your liability never exceeds the item’s market value, so you won’t face additional debt collection. If the sale generates more than your loan plus interest, the pawnbroker must return this surplus to you. Recent regulatory improvements have strengthened these protections significantly, ensuring fairer outcomes for borrowers.

| Scenario | Timeline | Financial outcome | Item status |

|---|---|---|---|

| Repay on time | Within 6-7 months | Pay loan + interest only | Jewellery returned immediately |

| Renew loan | Before deadline | Pay interest + any renewal fees | Jewellery held for extended period |

| Default | After deadline passes | No further liability beyond item value | Jewellery sold; surplus returned if applicable |

| Early repayment | Anytime before deadline | Reduced interest charges | Jewellery returned immediately |

Managing repayment effectively requires planning from day one. Set aside money regularly rather than scrambling at the deadline. If you receive unexpected income, consider early repayment to reduce interest costs. Monitor your loan expiry date carefully and contact the pawnbroker well in advance if you’re struggling. Early communication often leads to more flexible solutions.

Legal protections under FCA regulation significantly improve fairness. Pawnbrokers must treat customers fairly, particularly those in vulnerable circumstances. They can’t impose unreasonable charges or use aggressive collection tactics. If you believe a pawnbroker has treated you unfairly, you can complain to the Financial Ombudsman Service. These protections create a more balanced relationship between borrowers and lenders.

Tips for successful loan management:

- Set calendar reminders for repayment deadlines

- Budget for repayment from the moment you take the loan

- Communicate early if you anticipate repayment difficulties

- Understand renewal costs before committing to extensions

- Keep all documentation until the loan is fully settled

- Request written confirmation when loans are repaid

Explore jewellery care tips for 2026 to understand how proper maintenance protects your valuable pieces, whether in your possession or pledged as collateral.

Discover trusted pawnbroking services for your jewellery

When you need reliable, transparent pawnbroking services backed by decades of expertise, choosing the right partner makes all the difference. Blackwell Jewellers combines over 20 years of family-run experience with full FCA compliance, offering responsible cash loans on jewellery across Kent and nationwide.

Our expert valuers assess each piece fairly, considering current market conditions and intrinsic value. You’ll receive clear, written terms with no hidden fees or unexpected charges. We treat your jewellery with the same care we apply to our own authenticated collections, storing items securely throughout the loan period. Whether you hold gold, silver, diamond pieces or hallmarked antiques, our transparent approach ensures you understand exactly what you’re agreeing to. Visit our Maidstone, Gravesend or Bexleyheath locations, or contact us to discuss your pawnbroking needs with professionals who genuinely care about responsible lending.

FAQs about cash loans on jewellery

What is the maximum loan term for a jewellery pawn loan?

Most UK pawnbrokers offer loan terms of six to seven months as standard. You can often renew or extend this period by paying interest or arranging new terms before the deadline. Some pawnbrokers allow multiple renewals, though this increases total costs significantly.

Can I get a loan without a credit check when pawning jewellery?

Yes, pawnbroking requires no credit checks whatsoever. Your loan is secured against your jewellery’s value, not your creditworthiness. This makes pawnbroking accessible to people with poor credit histories or those avoiding traditional lending for personal reasons.

What happens if I don’t repay my jewellery loan?

The pawnbroker sells your jewellery to recover the outstanding loan and interest. Your financial liability is capped at the item’s market value, so you won’t face additional debt collection. If the sale generates surplus funds exceeding your loan amount, the pawnbroker must return this money to you under FCA regulations.

Are pawnbrokers regulated in the UK?

All legitimate pawnbrokers must be authorised by the Financial Conduct Authority under the Consumer Credit Act. Many also belong to the National Pawnbrokers Association, which enforces additional conduct standards. Always verify FCA authorisation before using any pawnbroking service.

How do I prove ownership of my jewellery?

Bring purchase receipts, insurance documents or previous valuation certificates if available. Whilst not always mandatory, ownership proof strengthens your position and may improve loan terms. Photo identification and proof of address are required regardless of whether you have jewellery documentation.